Leadership Made Simple

Building a “Want To” Culture

Leadership gets overcomplicated. People make it sound heavier than it is, harder than it is, and more mysterious than it is.

But real leadership is not about control. It’s not about pressure. And it’s not about having all the answers.

Real leadership is about creating the conditions where people want to give their best.

In the same way a conductor enables gifted musicians to make beautiful, majestic music, leadership is what enables a team, a business, or a movement to achieve greatness. The conductor does not play every instrument. The conductor creates alignment, clarity, timing, and belief. That’s what great leaders do.

At WealthWave, that matters more than ever. We’re not just building businesses. We’re building people. We’re advancing financial literacy. We’re helping families understand money so they can avoid exploitation and make better decisions for their future. That mission is too important for leadership to be confusing.

The good news is this: leadership doesn’t have to be hard.

In fact, the best leadership is often the simplest. It comes down to a few essential elements that, when consistently applied, create Accelerated Continuous Improvement. That means not just occasional wins, not just isolated projects, but ongoing progress that becomes part of the culture.

That is the goal, not temporary momentum, but lasting excellence.

Start With the Vital Few

One of the biggest reasons organizations lose energy is because they try to do too much at once.

People don’t get inspired by clutter. They get inspired by clarity.

Great leaders identify the vital few issues that matter most and bring the organization into focus around them. When everyone knows what matters most, distractions lose power. Activity becomes aligned. Effort becomes purposeful.

At WealthWave, that means every leader must be able to answer a simple question: what are we truly trying to accomplish right now?

If the answer is vague, the team will drift. If the answer is clear, the team can move.

A unifying theme gives people something bigger than a checklist. It gives meaning to the work. It reminds every team member that what they do matters, and that their effort connects to a larger purpose. People will always work harder for meaning than they will for management.

Create a “Want To” Culture

There’s a big difference between “have to” and “want to.”

“Have to” produces compliance.

“Want to” produces commitment.

Compliance may get you activity for a while. Commitment gets you discretionary effort—the extra thought, energy, creativity, and persistence people only give when they believe in what they’re doing.

That’s where real growth lives.

A “want to” culture is created when people feel three things: they know the mission, they understand their role in it, and they believe their contribution matters.

This is why leadership is not mainly about pushing. It’s about connecting.

When people are reminded that they are helping families become financially independent, helping parents teach their kids about money, helping people avoid the traps that come from ignorance, their work stops feeling like pressure and starts feeling like purpose.

Purpose energizes people in a way pressure never can.

Move Beyond Projects to Enterprise-Wide Improvement

Many organizations get excited about projects. Fewer build a culture of improvement.

Projects are fine. But projects end.

Culture stays.

If leadership is done right, improvement does not depend on one event, one promotion, one campaign, or one strong month. It becomes the way the organization thinks. The team starts looking for better ways to communicate, better ways to serve, better ways to duplicate, and better ways to lead.

That’s enterprise excellence.

For WealthWave leaders, this means improvement cannot live only in strategy sessions or leadership retreats. It has to show up in field training, in coaching, in meeting rhythms, in recruiting conversations, and in the way we recognize progress.

When improvement becomes normal, growth becomes sustainable.

Keep the Plan Clear and the Execution Simple

A good plan that people understand will outperform a brilliant plan that nobody can execute.

That’s another place where leaders make things too hard.

The right action plan is not complicated. It is clear. It tells people what matters, what happens next, who owns it, and how progress will be measured. It turns vision into movement.

People don’t need more noise. They need direction.

The best leaders simplify the path forward so their team can act with confidence. They remove confusion. They reduce friction. They help people see the next step and take it.

And just as important, they stay with it.

A launch is exciting. Maintenance is leadership.

Anybody can rally a team for a moment. Great leaders keep the team engaged long enough to create lasting change. They know that consistency is what turns a message into a mindset and a mindset into a culture.

When You’re Stuck, Go Back to the Purpose

Every organization hits dead ends. Every leader has moments when the path forward is unclear.

That does not mean progress is over. It means leadership is required.

When a team gets stuck, the answer is not always more effort. Sometimes the answer is better perspective. Sometimes it means narrowing the focus. Sometimes it means asking better questions. Sometimes it means inviting ideas from people who are closer to the challenge than the leader is.

Innovation often comes from clarity, not chaos.

When people understand the mission and the problem clearly, they start offering creative ideas that directly apply to the organization. They stop waiting to be told everything. They start thinking like owners.

That is what a healthy culture does. It unlocks the intelligence of the whole team.

Celebrate Success and Reinforce What Created It

Celebration matters.

Not because leaders need to flatter people, but because people repeat what gets recognized.

When a team member grows, when a leader duplicates, when a family is served well, when a breakthrough happens, it should be acknowledged. Celebration creates belief. It reminds people that progress is real. It turns momentum into confidence.

But strong leadership goes one step further.

It doesn’t just celebrate the outcome. It reinforces the behavior that created the outcome.

That’s how culture is built.

When leaders consistently point back to the habits, decisions, discipline, and teamwork that produced success, they teach the organization how to win again. Success stops being random. It becomes repeatable.

The Quality of Management Changes Everything

People can feel the difference between being managed poorly and being led well.

Poor management creates confusion, fatigue, and unnecessary friction. Strong management creates order, trust, and progress. It gives people confidence that their effort is going somewhere.

That’s why leadership matters so much. It shapes the experience people have inside the organization. It affects morale, retention, creativity, accountability, and results.

In short, leadership changes the slope of the line.

That’s the point.

The purpose of leadership is to accelerate improvement, to help people and organizations get better, faster, and in a way that lasts. Not through pressure, but through clarity. Not through complexity, but through focus. Not by forcing activity, but by building belief.

Final Thought

Leadership is not about making people do more. It is about helping people become more.

When you focus your organization on the vital few, align people around a meaningful mission, engage hearts as well as hands, execute with clarity, celebrate progress, and reinforce the right behaviors, you create the kind of culture every leader wants, a culture where people do not merely comply, they commit.

That’s a “want to” culture.

And when that culture takes hold, improvement is no longer occasional. It becomes continuous. Growth is no longer fragile. It becomes durable. Excellence is no longer an aspiration. It becomes the standard.

Leadership doesn’t have to be hard.

It just has to be clear, consistent, and connected to purpose.

And when it is, great things happen.

Because when people know why they matter, they will give you their best.

Why Clients Leave

And How WealthWave Leaders Can Build Unshakeable Loyalty

“The client who stays with you is the client who trusts you to protect their financial future. Lose that trust, and you lose them.”

Here’s the reality: clients will come and go. Some will move, retire, or simply drift away. That’s the natural ebb and flow of any business. But when clients leave because you didn’t show up, didn’t listen, or didn’t deliver on what you promised—that’s on you.

As WealthWave leaders, your mission isn’t just to educate people about money; when they become clients, it’s to keep them engaged, empowered, and confident in their financial decisions long after that first conversation. If you’re not actively working to keep clients satisfied and continuously adding value, you’ll find yourself in a never-ending cycle of chasing new business instead of deepening the relationships you already have.

Let’s get straight to it: Why do clients leave, and what can you do to stop it?

The Retention Reality Check

Here’s a sobering fact: research shows that 20% of clients who switch financial professionals do so within the first year, and another 25% leave within the second year. That means nearly half of your client turnover happens in those critical early stages—right when trust is being built or broken.

Why does this happen? Poor communication. Lack of follow-through. Mismatched expectations. Clients leave when they feel forgotten, confused, or underserved. And in today’s world, where people have endless options at their fingertips, they won’t hesitate to find someone who makes them feel valued.

The good news? You have complete control over this. Retention isn’t about luck—it’s about intention. It’s about how you show up, how you communicate, and how deeply you understand the people you serve.

The Great Wealth Transfer: A Massive Opportunity (Especially for Women Leaders)

Here’s something you need to pay attention to: we’re in the middle of the largest wealth transfer in history. Over the next two decades, an estimated $84 trillion will pass from Baby Boomers to the next generation. And here’s the part most people miss: a significant portion of that wealth is going to women.

Women are inheriting assets. They’re building businesses. They’re becoming the primary breadwinners. By some estimates, women will control nearly two-thirds of the nation’s wealth within the next decade. That’s a seismic shift in who makes financial decisions in America.

And here’s the kicker: Forbes reports that 94% of women who inherit wealth or come into significant assets want to work with a female financial professional. Ninety-four percent. Think about that for a moment.

Why? Because women want someone who understands their concerns, their goals, and their communication style. They want a professional who listens, educates, and partners with them—not someone who talks down to them or makes assumptions about what they need.

For WealthWave’s women leaders, this is your moment. You have a unique opportunity to serve a growing, underserved market that’s actively looking for someone like you. But you have to show up with intention. You have to communicate clearly. You have to educate relentlessly. And you have to build relationships that last.

This isn’t just about gender—it’s about connection, trust, and the ability to meet clients where they are. Women leaders who understand this will be positioned to capture a massive share of this wealth transfer. The question is: are you ready?

Six Reasons Clients Walk Away (And How to Fix It)

Let’s break down the most common reasons clients leave—and what you can do about each one.

1. You’re Not Communicating Enough (Or the Right Way)

Here’s a question: when was the last time you reached out to a client before they reached out to you?

Being responsive is good. Being proactive is better. If the only time clients hear from you is when they have a problem or when it’s time to review their account, you’re missing the point. They need to know you’re thinking about them, that you’re looking out for their best interests, and that you’re there before they realize they need you.

Consider this:

- Three out of five clients say more frequent, personalized contact would give them more confidence in their financial plan.

- 85% of clients factor communication style and frequency into whether they’ll stay with you.

- 75% want personalized updates—not generic emails blasted to your entire list.

The Fix: Build a communication plan and stick to it. Monthly check-ins. Quarterly reviews. Personal notes on birthdays or major life events. Tailor your message to each client. Make them feel like you’re speaking directly to them, not to everyone.

2. You’re Slow to Follow Up

People are busy. They lose momentum when you don’t respond quickly. Worse, they feel unimportant when their questions go unanswered or their requests sit in limbo.

When you’re working with someone’s financial future, delays create anxiety. They start wondering: Did they forget about me? Are they even paying attention? And if they’re new to working with you, a slow response can kill the relationship before it even starts.

The Fix: Set a standard for yourself—respond within 24 hours, even if it’s just to say, “Got your message, I’m looking into this and will have an answer by [date].” Show them you’re on it. Speed builds trust.

3. You’re Not Addressing What They Actually Care About

Here’s a disconnect that’s costing professionals clients: over 90% of people want help with estate planning, but only 22% are getting it from their financial professional. Eighty-nine percent want tax-planning advice, but only 25% receive it. And while 73% want guidance on charitable giving, just 2% are getting that support.

Why the gap? Because too many professionals are narrowly focused on investments and portfolios. But clients need more. They want a holistic approach—someone who understands their full financial picture and helps them make informed decisions across all areas of their life.

The Fix: Ask better questions. Find out what keeps them up at night. Revisit their goals regularly. Don’t assume you know what they need—ask them, listen, and deliver. At WealthWave, we’re educators first. Use that to your advantage.

4. You Let Market Volatility Blindside Them

Yes, market performance matters. But here’s the thing: most clients understand that markets go up and down. What they don’t understand is being caught off guard by a downturn without any context or reassurance from you.

The issue isn’t the numbers—it’s the lack of preparation and communication around those numbers. If clients feel like they were sold a dream that didn’t match reality, they’ll look for someone who sets better expectations.

The Fix: Educate your clients about how money works. Talk about historical market cycles. Explain volatility before it happens. When markets get rough, reach out proactively. Remind them of their long-term goals and the strategy you’ve built together. Reassurance goes a long way.

5. Your Technology Is Clunky or Outdated

We live in a world where people can order groceries, book flights, and manage their entire lives from their phones. If your client portal is slow, confusing, or outdated, you’re creating friction.

A recent survey found that 44% of clients are frustrated they can’t view all their investments in one place, and 49% choose firms based on the digital experience they provide.

The Fix: Make sure your tools work seamlessly. If your platform isn’t user-friendly, push for improvements or find partners who offer better technology. Your clients shouldn’t have to struggle to see their own financial information.

6. Your Fees Are a Mystery—Or Too High for the Value You Deliver

Clients expect to pay for quality service. But they also expect transparency. If they don’t understand what they’re paying for—or if they feel like they’re not getting value for the fees—they’ll find someone else.

The Fix: Be upfront about your fees from day one. Explain what they’re paying for and why it’s worth it. If you use specific tools or platforms, show how those add value. And make sure your service matches your pricing. If you’re charging premium fees, deliver a premium experience.

The Service Factor: Why Support Makes or Breaks Retention

Here’s something that doesn’t get talked about enough: your ability to retain clients isn’t just about what you do—it’s also about how well your headquarters supports you.

Think about it. When a client calls with a question and gets bounced around to voicemail, they get frustrated. When paperwork takes weeks to process, they start wondering if they made the right choice. When service requests sit unanswered, they lose confidence—not just in you, but in the entire organization.

Service quality is a retention driver. The faster, smoother, and more efficient the back-office support, the better you look to your clients. When headquarters answers the phones quickly, processes requests without delay, and makes it easy to do business, your job gets easier. You spend less time putting out fires and more time building relationships.

Here’s what excellent service looks like:

- Answer the phones. Real people, real answers, minimal hold time. When clients or leaders need help, they shouldn’t feel like they’re navigating a maze.

- Make it fast. Every day a request sits unprocessed is a day your client doubts the system. Speed isn’t just convenient—it’s a competitive advantage.

- Follow up relentlessly. If something requires additional steps, communicate that clearly and keep everyone in the loop. No one should have to wonder what’s happening with their request.

- Make it easier to do business. Simplify processes. Cut red tape. Eliminate unnecessary steps. The easier you make it for leaders to serve their clients, the better those clients will feel about the entire experience.

When WealthWave’s home office delivers exceptional service, it multiplies your effectiveness. When service is slow or inconsistent, it drags down retention no matter how good you are in the field. This is a partnership—and both sides have to hold up their end.

Bottom line: Push for excellence at every level. Hold headquarters accountable for fast, friendly, professional service. And when they deliver, make sure your clients know they’re supported by a world-class team.

Four Strategies to Build Unshakeable Client Loyalty

Now that you know why clients leave, let’s talk about how to keep them.

Strategy 1: Create a Communication Plan—And Actually Use It

Most client issues come back to communication. But it’s not just about talking more—it’s about saying the right things at the right time and truly listening.

- Make sure clients know you’re always available.

- Engage them regularly with updates, insights, and check-ins.

- Ask questions and follow through to show you’re listening.

- Be proactive, not just reactive.

Strategy 2: Position Yourself as an Educator, Not Just a Portfolio Manager

At WealthWave, we’re financial educators. That’s your edge. Your relationship with clients shouldn’t hinge solely on investment performance—it should be built on your ability to guide them through every stage of their financial journey.

- Focus on long-term goals, not just short-term returns.

- Build a personal relationship that extends beyond account balances.

- Offer education and resources that empower them to make better decisions.

Strategy 3: Engage Clients Beyond Their Accounts

Show your clients they matter to you as people, not just as portfolios.

- Host client appreciation events.

- Send personal notes for birthdays, anniversaries, or milestones.

- Offer to speak at their community events or groups.

- Support causes that matter to them.

These small gestures build loyalty that goes far beyond transactions.

Strategy 4: Leverage WealthWave’s Tools and Resources

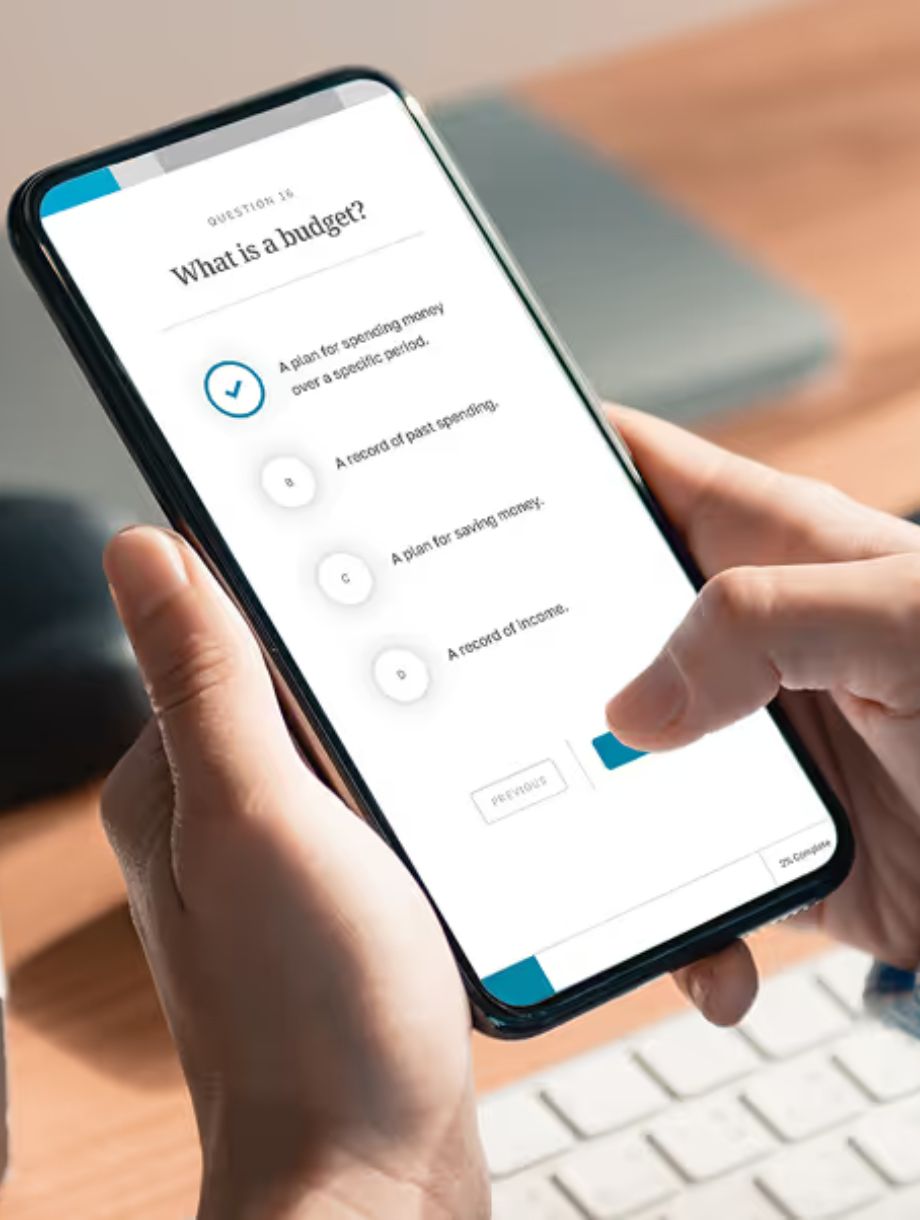

You’re not in this alone. WealthWave provides you with educational materials, technology, and support to help you deliver an exceptional client experience. Use them. Share TheMoneyBooks Series resources. Direct clients to howmoneyworks.com or taketheflq.com. Show them you’re part of a movement that’s raising financial literacy nationwide.

The Bottom Line

Clients don’t leave because of market downturns or one bad quarter. They leave because they feel ignored, confused, or undervalued. They leave when the relationship becomes transactional instead of transformational. And they leave when the service experience—from you and from headquarters—doesn’t meet their expectations.

Your job as a WealthWave leader is to prevent that. Communicate clearly. Follow through relentlessly. Educate continuously. Show up consistently. And demand excellence from every part of the organization that touches your clients.

We’re standing at the edge of the greatest wealth transfer in history, with trillions of dollars moving into the hands of people—especially women—who are hungry for financial education and guidance. They want someone they can trust. Someone who listens. Someone who empowers them to make informed decisions.

That someone is you.

“People don’t care how much you know until they know how much you care.”

— Theodore Roosevelt

Make them feel it. Make them see it. Make them know it. That’s how you build unshakeable loyalty—and that’s how you move the world toward a future where people understand money and make confident, informed financial decisions.

Now go build those relationships. Your clients—and your business—depend on it.

The Approval Trap

Why the Greatest Leaders Trust the Mission More Than the Applause

There’s a silent epidemic crippling leaders across every industry—and it has nothing to do with skill, strategy, or even competition.

It’s approval addiction.

The insidious need to be recognized, validated, and praised before you can believe in what you’re building. The compulsion to check the room for nods before you speak your truth. The hesitation before bold action because you’re waiting for someone else to tell you it’s okay.

Here’s what I know after decades in this business: The leaders who change the world don’t wait for permission. They don’t need a standing ovation to know they’re on the right path. They trust the mission more than the applause.

And right now, in this defining moment—the largest wealth transfer in history, the biggest leadership gap we’ve ever faced, a $60 trillion industry accelerating toward families who desperately need guidance—WealthWave leaders cannot afford to be held hostage by the need for approval.

The Science Behind the Trap

Let’s get straight about what approval addiction actually is.

Research published in leadership journals confirms what many of us feel but rarely admit: when you constantly seek external validation, your leadership loses authenticity. You start making decisions based on what others expect from you rather than what aligns with your values and vision.

According to Harvard Business Review, leaders who depend on constant approval at work make themselves hostages to other people’s subjective opinions—opinions that may have nothing to do with the actual quality of their work and everything to do with personal biases, circumstances, or politics.

Here’s the kicker: You’re giving someone power over you. Power over your confidence. Power over your decisions. Power over your ability to lead families toward financial freedom.

Psychology research reveals three devastating consequences of approval-seeking leadership:

- You surrender your power to others’ subjective opinions – Their validation becomes your metric for success, even when their judgment may be clouded by bias or irrelevant to your mission.

- You make your happiness dependent on external input – Instead of celebrating what you know you’ve accomplished, you wait anxiously for someone else to tell you it was good enough.

- You disconnect from your intuition – The inner voice that knows what families need, what’s right, what’s true—gets drowned out by the noise of seeking approval.

As leadership expert John Bailey writes, “When you lead for external validation, you’re playing a losing game. People can sense when you’re not being genuine, and you’ll lose trust, respect, and authority over time.”

“Care about what other people think and you will always be their prisoner.

— Lao Tzu

Let me tell you what happens when leaders fall into this trap.

They hesitate to teach families the truth about financial products because they’re worried about industry criticism. They soften their message about financial literacy being a human right because they don’t want to rock the boat. They second-guess the 7 Money Milestones, wondering if they need more credentials before they can confidently guide someone toward financial freedom.

They wait for permission that will never come.

And while they’re waiting, families are drowning. $1.2 trillion in credit card debt at 24% interest. Two-thirds of Americans failing basic financial literacy tests. Nearly 40% of adults with zero retirement savings. One in three Americans with less than $500 set aside for emergencies.

This is not the time for leaders who need to be liked. This is the time for leaders who need to serve.

The Confidence That Comes From Conviction

Here’s what separates leaders who change lives from leaders who chase applause: internal confidence rooted in mission clarity.

You don’t need anyone’s permission to teach a family how compound interest works. You don’t need industry validation to show someone how the Rule of 72 can either make them wealthy or keep them broke. You don’t need a committee’s approval to sit across from a nervous parent and explain how to protect their family’s financial future.

You need to know, deep in your bones, that what we do matters.

Research on intrinsic versus extrinsic motivation confirms this truth: leaders driven by internal purpose—autonomy, mastery, and mission—consistently outperform those chasing external rewards like recognition and praise. When you’re anchored to the why behind your work, you become unstoppable.

Self-Determination Theory, studied across decades of leadership research, shows that autonomy-supportive leaders—those who trust their mission and give their teams the same freedom—create environments where people thrive, perform at higher levels, and sustain engagement over time.

“It is not the critic who counts; not the one who points out how the strong person stumbles… The credit belongs to the one who is actually in the arena.”

— Theodore Roosevelt

You're in the arena.

Every time you sit down with a family and teach them how money works, you’re in the arena. Every time you help someone understand the Time Value of Money, you’re in the arena. Every time you guide a new entrepreneur through e2E and show them how to build a business instead of just earning a paycheck, you’re in the arena.

The critics? They’re in the cheap seats. They don’t hold licenses. They don’t sit with widows trying to figure out their next move. They don’t look into the eyes of young adults drowning in debt with no one to teach them a better way.

You do.

And the families who trust you—who trust you with their careers, who trust you with their money, who trust you with their dreams—they don’t need you to be liked by everyone. They need you to be certain. Confident. Unwavering in the truth you carry.

How to Break Free From Approval Addiction

If you’ve recognized yourself in this article, here’s how to reclaim your leadership:

1. Get curious about the root cause.

Ask yourself: Where does this need for approval come from? Was I taught to seek validation? When did I start believing someone else’s opinion mattered more than my own knowledge and experience?

2. Reconnect with your intuition.

After every client meeting, every presentation, every training—pause and ask yourself, How do I feel about what just happened? Your gut knows. Trust it before you look for external feedback.

3. Take inventory of your strengths.

You wouldn’t be here if you weren’t capable. Write down what you know. Write down what you’ve accomplished. Write down the lives you’ve changed. That’s your evidence. That’s your foundation.

4. Use objective feedback to grow; dismiss subjective opinions.

If someone says, “You didn’t cover X in your financial plan,” that’s objective—and valuable. If someone says, “I don’t think financial education really works,” that’s subjective nonsense rooted in their own limitations. Learn to discern the difference.

5. Don’t expect approval—see it as a bonus.

Do the work because the work matters. Teach families because financial literacy is a human right. Build your business because entrepreneurship is the path to freedom. If someone celebrates you along the way, great. If they don’t, keep moving.

“You wouldn’t worry so much about what others think of you if you realized how seldom they do.”

— Eleanor Roosevelt

This Is the Biggest Moment in the World’s Largest Industry

Let me put this in perspective.

We are in the middle of a $124 trillion wealth transfer. The financial services industry is accelerating toward $60 trillion by 2033. Nearly 38% of the current financial workforce is about to retire, leaving a leadership void of roughly 100,000 professionals.

And here’s the most important part: families are desperate for guidance. They don’t know how money works. Schools didn’t teach them. The industry has exploited them. They’re one emergency away from financial collapse, and they’re looking for someone—anyone—they can trust.

That someone is you.

Not the you who waits for approval. Not the you who hesitates until someone validates your message. Not the you who checks the room before you speak your truth.

The you who knows what we do changes lives. The you who understands that financial literacy is a human right. The you who sees a family struggling and refuses to walk away just because leading them might not win applause from people who never stepped into the arena.

“The only thing necessary for the triumph of evil is for good men to do nothing.”

— Edmund Burke

Financial illiteracy isn’t just an inconvenience. It’s a crisis. It’s stealing sleep, straining marriages, shrinking dreams, and keeping smart, hardworking people trapped in a system designed to exploit them.

You have the knowledge. You have the tools. You have the system. You have the mission.

What you cannot afford to need is approval.

The Call to Action

Here’s what I’m asking you to do right now—not tomorrow, not when you feel ready, not when someone gives you permission—right now:

Stop waiting for applause and start trusting the cause.

Go sit with that family who’s been on your mind. Teach them the financial formula that changes lives. Show them the Rule of 72. Walk them through the 7 Money Milestones. Give them TheMoneyBooks. Help them take the Financial Literacy Quiz and see where they stand.

And when you do, don’t look around the room for validation. Don’t check your phone for congratulations. Don’t wait for someone to tell you that you did a good job.

You’ll know you did a good job when you see the light come on in their eyes. When they finally understand how money works. When they realize they’re not broken—they were just never taught. When they take the first step toward financial freedom because you had the courage to lead them.

That’s your reward. That’s your recognition. That’s your standing ovation.

This is not the time to play small. This is not the time to shrink back because you’re worried about what people think. This is not the time to let approval addiction keep you from the greatest work of your life.

This is the biggest and most important moment in the world’s largest industry.

And it doesn’t belong to the leaders waiting for permission.

It belongs to the leaders who trust the mission more than the applause.

Are you one of them?

“Wealth follows literacy. Literacy changes lives.”

Now go change some lives. The world is waiting.

The Ripple Effect

How One Leader’s Impact Can Spread Across Generations

Financial literacy isn’t something I discovered—it’s in my DNA.

I grew up in a home where money conversations weren’t whispered behind closed doors or avoided at the dinner table. They were everywhere. My father was a CPA. My grandfather worked in finance. My grandmother and uncle dedicated their lives to helping people climb out of debt and rebuild their futures.

I didn’t just learn about money—I breathed it. I watched my family change lives, one conversation at a time, long before I understood what they were really doing.

In 1982, I made a decision that seemed small at the time but would prove to be the most consequential choice of my life:

I started in this business. All by myself.

No team. No reputation. No safety net. Just a young man with a belief that financial literacy could change the world—and the willingness to teach it to anyone who would listen.

That one decision—made over four decades ago—has impacted millions of people through today.

Between the companies we’ve started, the leaders we’ve developed, the clients we’ve served, the families we’ve educated, and the millions of copies of TheMoneyBooks series that have been read across America—the ripple is almost impossible to measure.

But here’s what I know for certain:

One decision. One day. One person willing to start.

And today, the world has changed because of it.

Not because I was the smartest. Not because I was the most talented. Not because I had advantages others didn’t.

But because I understood something my grandmother taught me when I was young:

“Tommy, when you teach someone about money, you don’t just help them—you help everyone they’ll ever love.”

She was right.

And every single day since 1982, I’ve watched that truth play out in ways that humble me, inspire me, and remind me why this work matters more than anything else I could ever do.

That one conversation I had in 1982—and the very first family I ever sat down with—started a ripple that is still moving today.

I’ll never know their great-grandchildren’s names. I’ll never see the college funds that were started because of a principle I taught. I’ll never hear the debt-free retirement parties that happened because someone remembered the Rule of 72.

But I know they happened.

And I know this: if one person, starting alone in 1982, can create a ripple that touches millions—so can you.

Because the ripple effect isn’t about being the best. It’s not about being the loudest or the most famous.

It’s about being willing to start.

And once you do, the ripple takes care of the rest.

“We make a living by what we get. But we make a life by what we give.”

— Winston Churchill

The Mathematics of Legacy: Why One Conversation Multiplies Forever

Most leaders think in terms of addition:

One appointment = one client.

One presentation = one sale.

One recruit = one team member.

But financial literacy doesn’t follow the rules of addition. It follows the mathematics of exponential multiplication—the same compounding principle we teach families every single day.

The Butterfly Effect in Leadership

In chaos theory, scientists discovered that rounding a single number by 0.000127 in a weather model produces completely different global outcomes weeks later. One tiny variation—invisible at first—changes everything downstream.

Leadership works the same way.

When you teach one family the Rule of 72, you’re not just impacting four people. You’re setting in motion a generational cascade:

Generation 1 (Year 0):

- 1 family learns (≈4 people impacted)

Generation 2 (Years 1–10):

- That family teaches 6 more families through referrals, conversations, and influence

- Total: 28 people impacted

Generation 3 (Years 11–25):

- Those 7 families teach 27 more families

- Total: 136 people impacted

Generation 4 (Years 26–50):

- Those 34 families teach 100+ families

- Total: 536+ people directly or indirectly impacted

Now multiply that by 50 families per year over a 10-year career:

500 families × 536 people per ripple = 268,000 lives impacted.

And you’ll never meet 99% of them.

Now imagine what happens over 42 years.

That’s not theory. That’s my life. And it can be yours.

The Three Types of Ripples You Create Every Day

1. The Knowledge Ripple

The principles you teach don’t die when the conversation ends. They become heirlooms—passed from parent to child, mentor to protégé, friend to friend.

- A single explanation of the Rule of 72 spreads across three generations.

- One family learns the 7 Money Milestones and teaches their children, who teach their children.

- A TikTok video you didn’t even know existed quotes TheMoneyBooks and reaches 2 million people.

Knowledge is the most durable form of wealth—and the only asset that multiplies when you give it away.

2. The Behavioral Ripple

People don’t just remember what you taught—they remember what you modeled.

When your team watches you:

- Prospecting with confidence every single day

- Serving families without needing applause

- Celebrating others’ wins louder than your own

- Leading with mission over money

They don’t just hear the lesson. They become the lesson.

And when they lead that way, their teams do too. Behavior compounds faster than advice ever will.

3. The Generational Wealth Ripple

This is where the mathematics get breathtaking.

Family A (no financial literacy):

- Generation 1: $50K in debt, no savings, financial stress

- Generation 2: Inherits the stress and the debt cycle

- Generation 3: Repeats the cycle

Family B (learns financial literacy from you):

- Generation 1: Eliminates debt, builds $500K in assets

- Generation 2: Inherits knowledge + $500K, builds $2M

- Generation 3: Inherits knowledge + $2M, builds $10M+

You didn’t just help one family. You rewrote the next century of their bloodline.

And they’ll never forget the leader who made that possible.

The Moment We’re In: Why Your Ripple Matters More Than Ever

Let’s talk about the opportunity in front of us—because the numbers are staggering:

The Wealth Transfer Crisis

- $124 trillion will change hands by 2048

- $87 trillion will go to women (many of whom have never managed wealth before)

- The financial industry is losing 38% of its workforce to retirement in the next decade

- We face a 100,000-leader shortage by 2034

The Financial Illiteracy Epidemic

- 66% of Americans cannot pass a basic financial literacy test

- 40% have zero retirement savings

- 60% live paycheck-to-paycheck

- $1.2 trillion in credit card debt compounds at 24% APY

- Financial illiteracy cost the U.S. $246 billion in 2025 alone

The Industry Explosion

- The global financial services market is $30+ trillion today

- Projected to hit $44 trillion by 2028

- And exceed $60 trillion by 2033

This is not hype. This is the largest wealth movement in human history—and the families who understand money will thrive, while those who don’t will be exploited, left behind, and buried in debt they’ll pass to their children.

Your ripple is the difference.

“We cannot live only for ourselves. A thousand fibers connect us with our fellow men; and among those fibers, as sympathetic threads, our actions run as causes, and they come back to us as effects.”

— Herman Melville

How to Maximize Your Ripple: Five Strategies That Multiply Legacy

1. Teach Principles That Can Be Taught Again

Don’t just solve problems—teach families how to solve them.

The Rule of 72, the 7 Money Milestones, TheMoneyBooks, and the Financial Literacy Quiz aren’t just tools. They’re transferable, teachable, repeatable systems that families can pass on.

Simple = scalable.

Complicated = dies with you.

2. Empower, Don’t Impress

Your job isn’t to be the smartest person in the room. Your job is to make the people you teach confident enough to teach others.

When a family leaves your table thinking, “Wow, Tom is brilliant,” you’ve created dependency.

When they leave thinking, “Wow, I can do this,” you’ve created a ripple.

3. Build Leaders Who Build Leaders Who Build Leaders

The leaders you develop will develop leaders. And those leaders will develop leaders.

I didn’t just recruit thousands of people. I mentored them until they could mentor others—and today, WealthWave has leaders in hundreds of communities across North America who have never met me but teach the same principles every single day.

That’s not a team. That’s a movement.

4. Document Your Wisdom

Write it down. Record it. Create resources that outlive you.

Books, videos, podcasts, one-pagers, scripts—these become heirlooms your team (and their teams) will use for decades.

TheMoneyBooks series has been read more than a million times—and every single copy is creating ripples I’ll never see.

5. Celebrate Every Ripple You See

When someone on your team helps a family, amplify it.

When a leader you trained develops a new leader, celebrate it publicly.

When you hear a second- or third-generation story, share it with everyone.

Celebration doesn’t just honor the win—it teaches the culture and accelerates the ripple.

The Invisible Legacy: Why You’ll Never Know Your Full Impact

Here’s the truth that will humble you and inspire you at the same time:

You will never know the full scope of your ripple.

You’ll never meet the teenager in 2043 who avoids $80K in student loan debt because her grandmother remembered something you taught in 2026.

You’ll never see the couple in 2038 who retires debt-free because a coworker shared a principle you taught their mentor in 2027.

You’ll never hear the eulogy in 2051 where someone says, “My father always taught us the Rule of 72—he learned it from a guy named Tom, and it changed our entire family’s future.”

But it will happen.

That is legacy.

And it doesn’t require fame, a stage, or a title. It requires one thing:

The courage to teach one family today—and trust the ripple to do the rest.

“The meaning of life is to find your gift. The purpose of life is to give it away.”

— Pablo Picasso

The Call: Start Your Ripple Today

Here’s your assignment—not tomorrow, not next week, today:

Step 1: Teach One Family One Principle

Sit down with a family (or call them right now) and teach them one core concept:

- The Rule of 72

- The 7 Money Milestones

- Why $11 trillion earning 0.40% while $1.2 trillion pays 24% is a crisis

- How compound interest works

Step 2: Ask Them to Teach Someone They Love

Before they leave, say this:

“You just learned something powerful. Will you teach this to one person you care about this week?”

That question activates the ripple.

Step 3: Repeat Every Single Day

One family. One principle. One request to pass it on.

Do that every day for five years, and your ripple will reach tens of thousands of lives.

Do it for 20 years, and your ripple will span generations you’ll never meet.

Do it for a lifetime, and your name will be whispered in gratitude long after you’re gone.

The Final Truth: Your Ripple Is Already Moving

If you’ve taught even one family how money works, your ripple has already begun.

Right now—this very moment—there are people making better financial decisions because of something you said, something you taught, something you modeled.

They might not remember your name. They might not know it was you. But the ripple doesn’t care about credit—it only cares about impact.

And in a world drowning in financial illiteracy, exploitation, and desperation, your ripple is the difference between a family that thrives and a family that drowns.

So teach.

Lead.

Serve.

Document.

Celebrate.

Repeat.

Because 50 years from now, when a young woman sits her daughter down and says, “Let me teach you something my grandmother taught me about the Rule of 72…”

That will be your legacy.

And it will be unforgettable.

Tom Mathews

WealthWave Women’s Survey 2026

This Isn’t Just a Survey. It’s Leadership.

At WealthWave, our mission is clear:

Erase financial illiteracy in America.

Financial literacy is not a luxury. It is not optional. It is foundational to freedom, stability, and long-term success.

In 2026, that mission takes a focused step forward.

The WealthWave Women’s Survey 2026 is now live. It represents more than ten questions. It represents awareness, preparation, and leadership.

A Historic Financial Moment

Over the next two decades, economists estimate that $124 trillion will transfer from one generation to the next.

The majority of that wealth will move into the hands of women.

This is not speculation. It is already happening.

Surviving spouses, daughters, and granddaughters will be entrusted with financial responsibility at an unprecedented scale. The question is not whether women will lead in this moment.

The question is whether they will feel equipped to lead confidently.

Preparation begins with education. Education begins with understanding.

That is why this survey matters.

What the Survey Is and What It Isn’t

The WealthWave Women’s Survey 2026 is:

- 10 multiple-choice questions

- Anonymous and confidential

- Designed to take approximately five minutes

It is not a sales tool.

It is not a pitch.

It is not about promoting a product.

It is about listening.

The questions explore:

- Financial confidence

- Primary money concerns

- Decision-making dynamics

- Areas where education is most desired

- The life stage women are currently navigating

When aggregated, these responses will create a national snapshot of how women are thinking and feeling about money today.

And data drives better decisions.

Why Financial Education Matters Now More Than Ever

For decades, financial literacy has not been consistently taught in schools. Many households avoided detailed financial conversations. Employers rarely provided practical education beyond retirement plan enrollment.

The result is predictable.

Hardworking individuals are navigating complex financial decisions without a structured framework.

For women, the stakes are even higher. Income disparities, career interruptions, caregiving responsibilities, and longer life expectancy all create unique financial dynamics.

Confidence does not come from guessing.

Confidence comes from understanding.

At WealthWave, we believe that when individuals understand how money works, they make stronger, more informed decisions. When people understand how cash flow functions, how debt impacts long-term growth, how compounding builds wealth, and how protection safeguards families, clarity replaces confusion.

This survey helps us identify where education is most urgently needed.

Listening Before Leading

Leadership begins with listening.

Before building new educational resources, before shaping public conversations, before appearing in media interviews or publishing white papers, we must understand what women are actually experiencing.

What are their biggest financial worries?

Where do they feel uncertain?

What do they most want to understand?

Who is currently leading major financial decisions in their households?

These answers allow us to focus our mission where it matters most.

Throughout 2026, the insights gathered from this survey will inform:

- Published research findings

- Educational initiatives

- Media conversations

- Community-level engagement

This is how change begins. Not with assumptions, but with clarity.

A Call to WealthWave Leaders and the Community

If you are part of the WealthWave community, this is your opportunity to lead.

Take the survey yourself.

Answer honestly.

Then share it with the women in your life:

- Family members

- Friends

- Colleagues

- Clients

- Neighbors

Invite them to contribute their voice to something larger than a single moment.

A simple invitation works:

“I just completed a quick anonymous survey about women and money. The results will help shape research and education throughout 2026. I would love for your voice to be included.”

No pressure.

No lecture.

Just participation.

Participation creates visibility.

Visibility creates awareness.

Awareness creates action.

Education Creates Confidence

At WealthWave, we believe:

Education creates confidence.

Confidence creates leadership.

Leadership transforms families and communities.

Financial literacy is not about selling products. It is about empowering individuals to make informed decisions.

This survey is one step in that larger movement.

Ten questions may seem small.

But when thousands of women answer honestly, the collective insight becomes powerful.

2026 can be a defining year for women and financial leadership.

It begins with listening.

Take the WealthWave Women’s Survey 2026

Add your voice.

Help shape the conversation.

Be part of the movement to erase financial illiteracy.

👉 Take the survey here:

https://form.jotform.com/253574555469067

Leadership starts with awareness.

And awareness starts with you.

Dow 50,000

History Made Today And What Leaders Do Next

On Friday, February 6, 2026, the Dow Jones Industrial Average closed above 50,000 for the first time in history, finishing at 50,115.67.

That number dominated headlines.

But leaders know the bigger story is not the number.

It’s the behavior that got us here, and the behavior that will carry families through whatever comes next.

Milestones don’t make people wealthy. Behaviors do. Teach the behaviors every day, especially when headlines get loud.

I Started in This Business When The Dow Was Under 1,000

I entered this industry in 1982, in a world that felt unstable: recession pressure, brutal interest rates, and a stock market that had gone nowhere for years.

Then on August 12, 1982, the Dow hit 776.92.

From that low to 50,000 is a generational reminder of a simple truth:

Time rewards discipline. Noise punishes emotion.

Peaks, Valleys, And The Real Lesson

1987: Panic tests conviction

On October 19, 1987, the Dow fell 22.6% and closed at 1,738.74.

The lesson: the market can scare you. Your plan must not be scared.

2000: Euphoria tests humility

The Dow closed at 11,722.98 on January 14, 2000 as the dot-com era crested.

The lesson: great markets do not remove risk. They hide it.

2002: Reality tests patience

The Dow later hit a closing low of 7,286.27 on October 9, 2002.

The lesson: quality and consistency beat prediction.

2009: Fear tests courage

During the Great Recession, the Dow’s lowest close was 6,547.05 on March 9, 2009.

The lesson: people do not need a forecast. They need leadership.

Every valley is a class. Every peak is a test. Teach people to pass both.

What Dow 50,000 Means And What It Doesn’t

It means progress compounds

Over long stretches, innovation, productivity, earnings, and human ambition push markets higher.

It does not mean risk is gone

Corrections and bear markets are not bugs. They’re features of investing.

It means the playbook still works

Save consistently

Build emergency reserves

Protect the foundation

Diversify growth

Rebalance when drift happens

Stay invested through the cycle

A headline level never built wealth. Automatic behaviors did: save first, own great businesses, reinvest, repeat.

Your Dow 50,000 Leadership Checklist

Run a same-day huddle

Tell your team: 50,000 is a mile marker, not a finish line.

Teach the timeline

Use the moments above to normalize volatility and train calm decision-making.

Tune the plan, not emotions

Rebalance if needed. Update goals. Adjust contributions. Do not chase headlines.

Increase automatic savings 1–2%

Use the moment to move people from intention to automation.

Turn attention into mission

Record highs open minds. Invite guests to a Financial Literacy Night and teach them how money works.

Make education the loudest voice

On big market days, families hear noise all day long. They need one clear voice. Yours.

When markets set records, set standards. Be the clearest voice clients hear that day.

Simple Talking Points For Teams, Clients, And Media

Context beats hype. “Dow 50,000 reflects decades of progress, not one day of luck.”

Staying power wins. “The investors who won were not the ones who guessed right. They were the ones who stayed consistent.”

Volatility is normal. “We’ve lived through crashes and recoveries. The plan is built for both.”

Education is the edge. “Financial literacy turns fear into discipline. Discipline lets compounding do its work.”

The Close

Dow 50,000 is not a victory lap.

It’s proof that time, ownership, and consistent saving beat every news cycle.

So today, celebrate the milestone. Then do what leaders do.

Invite them. Teach them. Protect them. Invest them. Stay with them.

And make this your call to action:

Run a “Dow 50,000” Special Session

Challenge every guest to:

Take the Financial Literacy Quiz at TakeTheFLQ.com

Start or increase automated savings

Meet with a WealthWave financial professional to put protection and investing on autopilot

Milestones grab attention. Leaders convert attention into action.

Tom Mathews

The Long Arc Of Financial Education

How Language And Money Built Civilization And Why We’re Finally Able To Close The Gap

Every time a family sits at a kitchen table and says, “We should be doing better than this,” they’re not confessing a lack of effort.

They’re confessing a lack of education.

That’s not an insult. It’s a historical reality.

For most of human history, financial education has been scarce, local, slow, and unevenly distributed. The people who understood money had leverage. The people who didn’t often paid for that gap in ways they couldn’t even name.

We live in a moment where that can change, because two forces that shaped civilization from the start are now converging again:

Knowledge (how it moves from one mind to another)

Money (how value moves from one person to another)

When you understand the history of those two “transfer systems,” you understand why financial illiteracy became normal, why it is profitable for the marketplace, and why leaders like you can finally help fix it at scale.

The Two Engines Of Human Progress: Language And Money

If you had to name the biggest invention of all time, it isn’t a machine.

It’s language.

Language is the first great technology because it allows something that changes everything: the transfer of knowledge. Once humans could share ideas precisely, everything else became possible.

And right alongside it, another “invention” changed what humans could build together: money.

Money is more than currency. It is a medium of exchange and a store of value that makes specialization possible. Without it, civilization stays stuck in barter, limited by coincidence and necessity.

If all you can do is barter, your world stays small.

If you can store value and exchange it reliably, your world expands.

Money made it possible for society to value things that are not immediately edible or tradable in a direct swap: poetry, craftsmanship, engineering, art, architecture, invention, education.

So here’s the big idea:

Language transfers knowledge. Money transfers value.

When those two systems work well, people advance.

When they work poorly or unevenly, people get exploited.

How Knowledge Moves: Three Elements That Decide The Future

Knowledge transfer always requires three elements:

The Owner Of Knowledge

The Receptor Of Knowledge

The Medium For Communication

The medium matters more than most people realize, because it determines four things:

Speed: how fast it spreads

Scale: how many people can receive it

Fidelity: how accurately it stays intact

Longevity: how well it survives generations

When you look at history through that lens, financial education wasn’t “ignored.” It was bottlenecked by the medium.

The Evolution Of The Medium: Why The Medium Is The Multiplier

1) Oral Conversations

Oral history is powerful, but it’s limited.

It’s mostly one-to-one.

It requires proximity and time.

It’s vulnerable to distortion.

It dies with the storyteller unless repeated faithfully.

Oral transfer required language, and language was the gate. But once language existed, humans could do something that changed the world again.

2) Written Communication

Writing lets knowledge outlive the speaker.

It becomes:

portable

preservable

repeatable

But early writing still moved slowly and stayed elite. If you had to copy something by hand, the “printing press” was your wrist. That is not scalable.

3) Printing

Printing wasn’t just a technology upgrade. It was a distribution revolution.

Suddenly:

one-to-many became normal

repetition became reliable

literacy became a pathway to power

But printing still had limitations: access, cost, gatekeepers, and slow feedback loops. A bad idea could spread, and a correction might take a generation to catch up.

4) The Internet

The internet removed the biggest historic constraints:

distribution cost collapsed

speed became instant

scale became global

multimedia became normal (text, video, voice, interactive tools)

Now the medium can finally match the mission.

And that matters because financial education is not just “information.” It’s confidence. It’s clarity. It’s language for life decisions. It’s the ability to see consequences before they happen.

Money As A Medium: Why Currency Changed Everything

If language is the medium that transfers knowledge, money is the medium that transfers value.

Without money:

trade stays limited to barter

specialization stays small

long-term planning stays fragile

“non-essential” cultural contributions struggle to survive

Currency allowed:

saving for the future

funding long projects

measuring value consistently

building systems that outlast a lifetime

And it also created a new reality:

If money is a medium, then understanding money is a form of literacy.

That’s why financial education is not optional. It is foundational.

Why Financial Education Isn’t Taught In Schools

Let’s be direct.

Financial education is not absent because it’s unimportant. It’s absent because it’s inconvenient, contested, and structurally orphaned.

Here are the biggest reasons:

1) The Curriculum Is Crowded And Testing Drives Decisions

Schools teach what gets tested. Personal finance is often treated as “life skills,” which tends to mean “nice, but not essential.”

2) Money Is Politicized And Culturally Sensitive

Teach budgeting and you’re safe. Teach debt, interest, investing, insurance, taxes, and behavioral traps, and you step into ideology, regulation, and controversy fast.

3) Teachers Are Rarely Trained For It

Most educators never received formal training in personal finance either. Schools can’t scale what they don’t confidently know how to teach.

4) The Real World Changes Faster Than Textbooks

Products evolve. Fraud evolves. Technology evolves. Rules evolve. The pace of the marketplace is faster than standard curriculum cycles.

5) No One “Owns” The Problem

This is the silent killer. Financial education sits in the gap between:

parents who assume schools will teach it

schools that assume parents should teach it

employers who benefit from productivity, not literacy

industries that profit whether consumers understand or not

When a problem has no clear owner, it becomes everyone’s problem and nobody’s responsibility.

The Profit In Confusion And The Cost Of Not Knowing

You said it plainly, and you’re right in principle: financial illiteracy is profitable.

Not because every company wakes up plotting against families, but because systems naturally reward the side that understands the rules.

Here’s what “profit from illiteracy” looks like in real life:

- interest paid for years because someone didn’t understand the cost of carrying balances

- fees and penalties triggered by confusion, not rebellion

- underinsurance or wrong coverage because the language felt overwhelming

- bad decisions made in panic because no one taught emotional discipline around money

- scams that succeed because the victim didn’t have a mental filter for what’s real

- decades lost because someone didn’t understand time, compounding, and risk

And the most painful part is this:

Most people don’t realize what happened until after the consequences compound.

That’s why education is protection. It’s also why education is leadership.

Why This Situation Can Finally Be Fixed

For the first time in history, the medium is strong enough to solve the problem at the scale the problem exists.

Here are the game-changing factors:

1) Instant Distribution

A message can reach a million people without a million conversations.

2) Multimedia Learning

Some people learn by reading. Some by listening. Some by watching. Now we can teach in every mode.

3) Shareability

The receptor of knowledge can instantly become an owner of knowledge and pass it on. That’s how movements spread.

4) Repeatability And Consistency

A standardized message reduces distortion. It protects quality. It preserves accuracy.

5) Community And Coaching

Education sticks when there’s accountability, repetition, and relationship. That’s what leaders provide.

This is where WealthWave matters.

Because the issue is not that Americans are lazy. It’s that they were never given a clear, repeatable money education framework they could understand and share.

WealthWave exists to close that gap.

What WealthWave Leaders Do Next

If the crisis is knowledge transfer, then the solution is leadership transfer.

Here are the commitments that separate “good intentions” from real impact:

1) Master The Message

You don’t need more hype. You need more clarity.

Learn the story. Internalize it. Personalize it. Say it in a way that sounds like you, but keeps the truth intact.

2) Teach In Short, Repeatable Conversations

Financial education wins in real life when it is:

simple enough to repeat

short enough to start

strong enough to matter

A 5–10 minute walk-through can change a trajectory if it becomes the first step into a new understanding.

3) Use Modern Mediums To Multiply Yourself

A flipbook. A short video. A shareable tool. A one-link resource.

That’s not “marketing.” That’s scalable knowledge transfer.

4) Protect The Purpose

We don’t lead with products. We lead with education.

Because when you teach people how money works, they start asking better questions. And better questions lead to better decisions.

5) Make It Practical

People don’t need a lecture. They need a path.

Help them take one next step:

learn a concept

fix a leak

ask a question

build a habit

create a plan

Education turns fear into action.

The Leadership Standard

You are not just building a business.

You are restoring something civilization has always needed: the fair transfer of life-changing knowledge.

Language made it possible to share wisdom. Money made it possible to build futures. Financial education is where those two meet.

And the moment you realize that, you stop seeing this as “content” and start seeing it as what it is:

a rescue mission for millions of families who never got the rulebook.

One quick note: Everything we teach should remain education, not personalized financial guidance. The goal is clarity and confidence so people can make informed decisions and seek the right professional support for their situation.

Closing Thought

“A society becomes wealthy when the many understand what the few have always known.”

That’s what we’re here to do.

Education first. Always.

The Financial Education Revolution

This Is the Moment We Were Built For

There are seasons when a business grows because you get better at what you do.

And then there are seasons when a business grows because history hands you a moment.

We are in one of those moments right now.

Not because the world suddenly got easier.

Not because the financial industry finally decided to reward families.

But because the gap has grown wider, the pressure heavier, and the cost of not understanding money more severe than ever.

People are working harder.

They’re earning more.

And yet they feel more uncertain about the future than the generation before them.

That’s not a coincidence.

It’s the result of a system that never taught them the rules.

Most People Were Never Taught How Money Works

Money touches nearly every decision we make for decades. Where we live. How long we work. How much stress we carry. Whether we feel confident or anxious about the future.

And yet, most people were never taught how money actually works.

Not in school.

Not growing up.

Not at work.

So they do what anyone does without a system.

They guess.

They react.

They copy what they see around them.

They hope things work out.

Hope, however, is not a strategy.

Education is.

Why WealthWave Exists

WealthWave exists for one reason: to teach people how money works, because most were never taught.

We don’t lead with products.

We don’t start with solutions.

We don’t try to convince people of anything.

We teach first.

If someone wants help applying what they learn, we can serve them. But education always comes first. That posture changes everything. It lowers resistance. It raises trust. It turns confusion into clarity.

When people understand how money works, money stops feeling mysterious. It becomes measurable.

This Is a Defining Moment

Families today are facing longer retirements, higher costs, more complex decisions, and more financial pressure than ever before. At the same time, financial literacy remains largely absent from everyday life.

That combination creates a defining moment.

Not a moment for panic.

A moment for leadership.

People don’t need more motivation. They need a map.

That’s why financial education matters more now than at any point in modern history. And that’s why WealthWave is not just growing a business. We’re leading a movement.

The Golden Apple

For centuries, the apple has symbolized education.

Gold has always symbolized wealth.

Put them together and you get a single image that captures everything we believe.

The Golden Apple.

We believe wealth follows literacy. And literacy changes lives. Families don’t fail because they’re lazy or irresponsible. They fail because they were never given the rules of the game.

Change the education, and you change the outcomes.

Teaching First Builds Trust

When you approach someone like a salesperson, they brace.

When you approach someone like a guide, they breathe.

Our educators are not pitching a sale. They’re handing someone a flashlight. Helping them see what’s happening in the financial world and where they fit inside it.

That’s why this movement resonates. It feels clean. It feels purposeful. It feels overdue.

Financial Literacy Is a Human Right

If people are expected to make lifelong financial decisions, they deserve to understand them. Financial literacy should not be a privilege reserved for insiders. It should be a basic life skill.

When people finally learn how money works, one thing becomes clear very quickly: the problem was never their effort. The problem was the absence of education.

Don’t Watch History. Step Into It.

A defining moment does not reward the most talented.

It rewards the most committed.

WealthWave is committed to teaching first, leading with integrity, and helping families find what they were never given.

This is the financial education revolution.

And this is the moment WealthWave was built for.

Tom Mathews

What Indiana Football Teaches Us

The Portal Moment In WealthWave

Hard Rock Stadium is loud in a way you feel in your ribs.

Indiana is protecting an undefeated season and a national title is sitting right there, one possession away. The safe decision is the obvious one. Kick. Take points. Don’t make a mistake.

Then the head coach makes a different choice.

He waves off the safe option and keeps the offense on the field.

Because champions do not build their future on fear.

Fourth-and-4. The call comes in. Fernando Mendoza takes the snap and runs like every “no” he ever heard is chasing him. He fights through contact, stretches, and breaks the plane. Touchdown.

Indiana seals perfection.

And the twist that makes it feel like a movie is where it happens: Miami. In Miami’s stadium. Against the program that once didn’t give Mendoza a shot.

What goes around comes around.

Dreams do come true.

The Hire That Started A Different Story

A year earlier, Indiana was a punchline. 3–9. The kind of season that makes people shrug and say, “That’s just who we are.”

Then Indiana hired a coach most people didn’t throw a parade for. Not a flashy name. Not a headline grabber.

But he walked into Bloomington with one rare thing that changes everything.

He already believed they could win big, and he was willing to demand that belief from everybody else.

That’s where turnarounds start. Not in the playbook. In the ceiling people carry around in their heads.

The First Thing He Changed Was Thinking

Before he changed the roster, he changed the room.

He attacked the quiet losing habits that hide in plain sight:

- hoping instead of expecting

- excusing instead of executing

- being “realistic” instead of being relentless

He made winning feel normal in practice before it ever showed up on Saturday.

That is leadership.

Not hype. Not speeches. Standards. Reps. Accountability. A clear message that said, “We are not doing it the old way anymore.”

The Transfer Portal Was Not About Stars. It Was About Hunger.

Then he used the modern tools: the transfer portal and NIL.

Here’s the part most people miss.

The portal is not only about stealing starters. A huge part of it is about finding second- and third-string players who are good enough, driven enough, and tired of waiting for permission to become who they know they can be.

Players with something to prove.

Think of all the talent in the world that sits on benches because of politics, timing, and somebody else’s name being bigger.

Those players are not “less than.” They’re just under-used.

And the right coach sees that as gold.

Mendoza’s Leap Was The Real Turning Point

Mendoza’s story is the kind leaders should study.

He grew up around Miami. He wanted that program. He tried. He didn’t get the spot he dreamed about. Then he went to Cal, played, developed, and still felt the limit.

Not because he lacked ability.

Because the path he was on could not take him where he wanted to go.

He wanted both: to play and to win it all.

So he did something that takes guts.

He chose a new team.

He entered the “portal,” took a chance on Indiana, and bet on a coach who was building something bigger than tradition.

And a lot of other players made the same bet.

They did not know what would happen.

The coach did.

The Season That Changed The Program

One year it was 3–9. Then 11–2. Then the story no one saw coming: 16–0, a national championship, and Mendoza lifting the Heisman.

That is not a “lucky year.”

That is what happens when belief turns into behavior, and behavior turns into results.

Indiana did what America has done at its best. It took people who were overlooked somewhere else, gave them a real chance, and built something unstoppable.

Not because they were castoffs.

Because they were unchosen potential.

The Financial Industry Doesn’t Have A Transfer Portal, But The Effect Is The Same

Now bring this home.

In the financial industry, there is no official transfer portal.

There’s no website where professionals enter their name and announce they’re ready for a new team.

But the reality is identical.

Every day, financial professionals sit in organizations where:

- their upside is capped by comp grids

- their growth is limited by politics and hierarchy

- their clients get treated like transactions

- their best ideas get buried under bureaucracy

- they feel like they’re “playing,” but not really building

They are talented. They are driven. They are proven.

They just need a chance to run the right system with the right team.

And at some point, they realize something that hits hard:

The opportunity they’ve dreamed about might not be where they are.

It might be one decision away.

Why WealthWave Can Be That Decision

WealthWave, at its best, is not “another place to work.”

It’s a platform for people who want a bigger outcome and are willing to grow into it.

A new team. A better development environment. A leadership culture that expects more. A model that lets professionals build something real, with mentorship, systems, and a mission bigger than a product.

For the right person, the move to WealthWave is not a lateral change.

It can be the moment they finally stop waiting for permission.

The moment they stop being “second string” in someone else’s system.

The moment their career stops being about surviving the season and starts being about winning it.

What WealthWave Leaders Should See In This Story

If you lead at WealthWave, this Indiana story is not just a feel-good sports moment.

It is your recruiting blueprint.

Because the people who change everything are often not the loudest stars in the room. They are:

- the advisor who is tired of being boxed in

- the leader with results who is ready to build, not just produce

- the quiet competitor who has been doing the work without getting the shot

- the professional who wants meaning, not just money

- the person who knows they have more, but needs a system that pulls it out

Your job is to see them before everyone else does.

Your job is to offer them what Mendoza found: belief, standards, and a real runway.

The Question That Decides Everything

Indiana didn’t magically become champions.

They changed coaches. They changed expectations. They changed the roster with hungry talent. They changed the outcome.

New team. Improved game. Different result.

So here’s the question this story asks every financial professional, and every WealthWave leader who recruits them:

Are you in the right system for the person you’re capable of becoming?

Because if you’re not, the next championship season of your life might not require more effort.

It might require a better team, a clearer mission, and the courage to step into your own “transfer portal” moment.

And when that moment comes, the leaders who win are the ones who do not settle for safe.

They go for it on fourth-and-4.

The Rule of 100 Hours

The Tiny Daily Habit That Brings Leaders Into the Top 5%

Most people don’t fail because they lack talent. They fail because they don’t build the time deposit that talent requires.

That’s why the Rule of 100 Hours is so powerful, especially for WealthWave leaders.

Here it is in plain terms:

If you spend 100 hours a year practicing a skill, you’ll become better at it than 95% of the population.

And the best part is the math: 100 hours a year is only 18 minutes a day.

Not two hours. Not “when life calms down.”

Eighteen minutes. Every day.

That’s the difference between hoping for growth and earning it.

“You don’t rise to your goals. You fall to your habits.”

— James Clear

Why This Matters in WealthWave